Policy Matters: “Risk on” driven by policy pivoting, expect more to follow

16-11-2022

There has been a dramatic change in market sentiment over the last two weeks, with policymakers in China unleashing different sets of policy support for private property developers. In addition, while the country is still maintaining its rhetoric on the “dynamic zero-Covid policy”, it also released measures to fine-tune the policy. These, together with the lower-than-expected CPI figures in the US last month (which ignited renewed expectations of monetary policy pivoting in the US), have stimulated a strong “risk on” momentum in the China stock market.

Our views:

We are positive about the policy developments. Our concerns over the two key China GDP components – domestic consumption and property – have certainly seen some relief after the recent policy announcements.

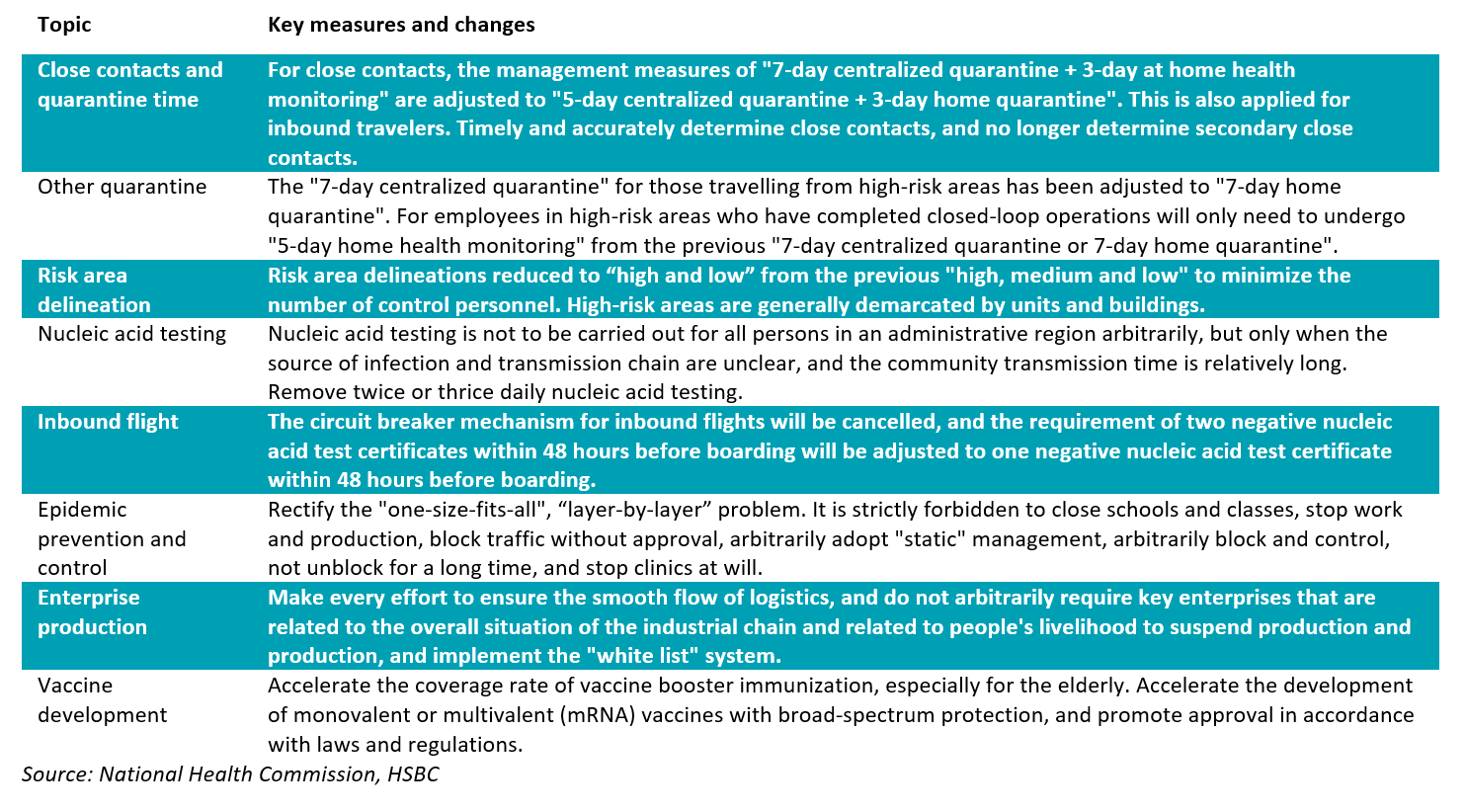

- On the consumption front, which the pandemic has dragged: The fine-tuned measures on anti-Covid controls, including the rectification of the “one-size-fits-all” and “layer-by-layer” problems and the 20 calibrating measures released by the National Health Commission (Exhibit 1), offer some early signs of loosening of zero-Covid. However, we view that a full exit of the policy is still a lengthy and gradual process. Our conviction in consumption recovery is supported by the recent reopening sign, which is an essential catalyst to benefit consumer companies and affiliated sectors down the value chain.

- On property: Previous easing measures were primarily rolled out at the local level and were focused on “guaranteeing the delivery”. The recent step-up in the supportive measures may directly support the liquidity and funding conditions of private property developers. These include the RMB 250 billion refinancing from the PBOC to support the bond financing (of private companies) and the 16 measures announced by the financial regulators to support the healthy development of the housing market (Exhibit 2).

- However, we note that although the share prices of property developers have bounced back strongly on the back of these developments (and particularly after a long, extended period of share price weakness), the long-term agenda of preventing the sector from a “hard-landing”, demographic changes in China, as well as the growth dynamics in the “new era” (economic modernization) should structurally promote a more sustainable and stable growth, contrary to the more vigorous growth in previous cycles.

Outlook:

Overall, we believe these positive policy changes have justified the recent stock market rally and reflect China’s strong and continued commitment to focus on economic growth. These also help address some of our and the market’s concerns. Moreover, the stabilized external environment, including the likely peaking of US inflation, a softer US dollar, as well as the direct dialogues of the top political leaders in the G-20 also helped improve market sentiment. Looking ahead, China’s weak macroeconomic data in October 2022, including the YoY decline in retail sales, suggest more supportive measures may follow to bolster the growth recovery.

From a valuations point of view, despite the recent rally, stock market valuations remain compelling. The Hang Seng Index is still trading around 7x PE, which remains well below its past 10-year average of 11x. Similarly, the MSCI China Index is trading at a PE of nearly 10.6x, which is below the 10-year average of 13x.1 These indicate that there is still room for ample upside.

Admittedly, there are still many uncertainties ahead, including the policy stance of the US Federal Reserve, as well as the potential back-and-forth of easing policies in China. While we will continue to monitor these closely and diligently, we are constructive that GDP and corporate earnings growth should pick up meaningfully in China next year. Meanwhile, our portfolio holdings – which primarily consist of the high-quality listed companies in the region, many of which are the solid leaders in the consumption, technology, and financial sectors – have benefited from the recent market rebound and remain well-positioned to ride through the market volatility and capture structural, secular growth potentials ahead.

Source:

- Bloomberg, 16 Nov 2022

Exhibit 1: Key measures and changes in the 20 measures to optimize the anti-Covid controls

Exhibit 2: 16 measures to support the healthy development of housing market

The views expressed are the views of Value Partners Hong Kong Limited only and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All materials have been obtained from sources believed to be reliable as of the date of presentation, but their accuracy is not guaranteed. This material contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investors should note that investment involves risk. The price of units may go down as well as up and past performance is not indicative of future results. Investors should read the explanatory memorandum for details and risk factors in particular those associated with investment in emerging markets. Investors should seek advice from a financial adviser before making any investment. In the event that you choose not to do so, you should consider whether the investment selected is suitable for you.

This commentary has not been reviewed by the Securities and Futures Commission of Hong Kong. Issuer: Value Partners Hong Kong Limited.